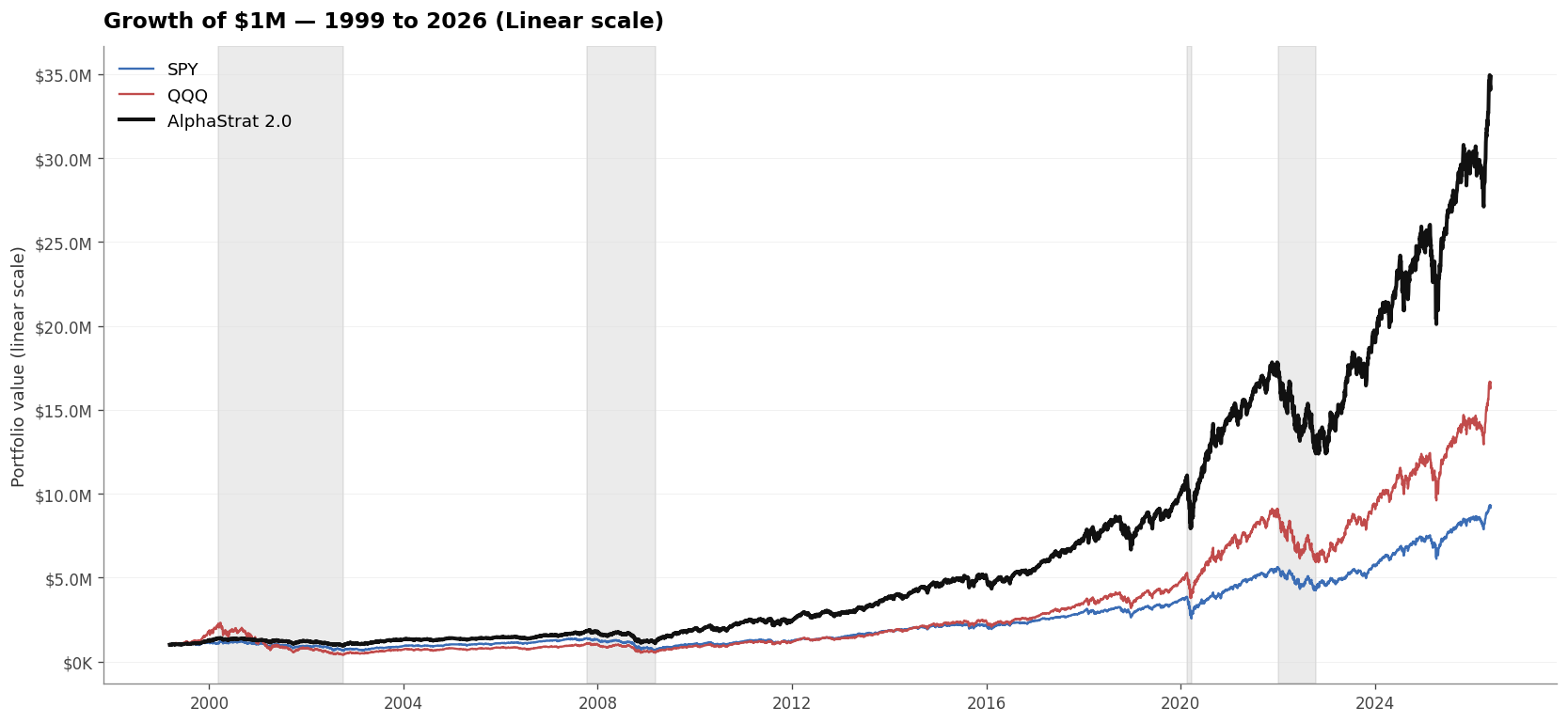

AlphaStrat 2.0 is the simplest investment rule I know how to build, and I've been building these for a while. It owns two things: shares of QQQ, the Nasdaq-100 fund, and BIL, a fund that holds short Treasury bills and pays you a few percent a year for parking your money there. And it follows one rule: keep the QQQ pile growing at 18% a year on paper.

Now, 18% is a tall order. Neither I nor anybody else can promise that QQQ will actually deliver 18% a year going forward. But the rule doesn't care about promises. It just looks at where QQQ ought to be if it had been keeping up with the line, and where it actually is. If QQQ has slipped behind, the rule sells some BIL and buys more QQQ. If QQQ has gotten ahead of itself, the rule takes a little off the top and parks it back in BIL. Same rule in 1999 as in 2026. A computer does it. No phone calls.

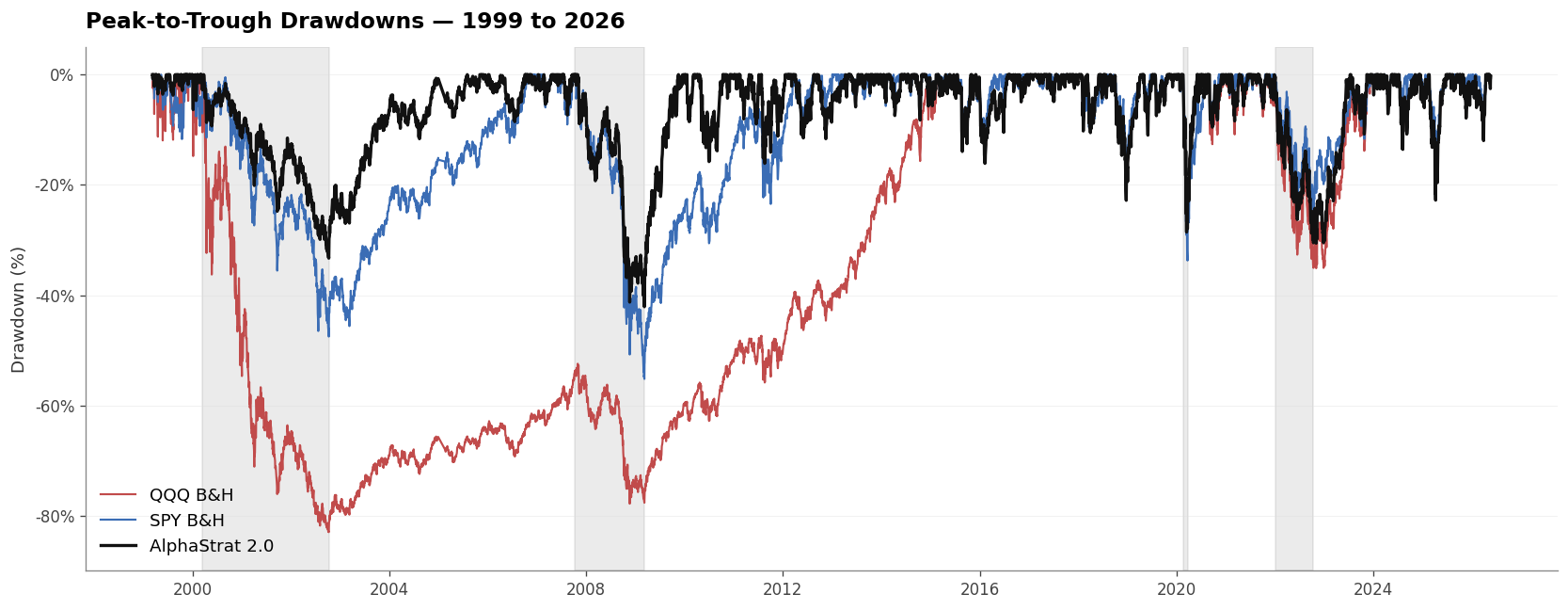

The setup is straightforward. On day one, you put thirty cents of every dollar into QQQ and seventy cents into BIL. That's a big cash cushion — bigger than most professional investors would tolerate. The point of the cushion is to have something to spend when QQQ goes on sale, which it does every five or ten years like clockwork. In 2002 the cushion bought QQQ at about $25 a share. In 2009 it bought it again. In 2022 it bought it once more. Each time, the math said the shares were cheap relative to where the line said they should be. The rule didn't argue. It bought.

Here is the result. From March 1999 through May 2026 — a stretch that included the dot-com unwind, the 2008 banking crisis, COVID, the 2022 sell-off, and three roaring bull markets — a million dollars handed to the rule on day one would be worth about $34.8 million today. The same million in QQQ would be $16.6 million. That works out to 14% a year compounded for the rule, 11% for QQQ. After the taxman takes his cut at top federal rates, the rule still compounds at 13.8% a year, while QQQ buy-and-hold drops to 9.9%. The worst stretch the rule lived through was a 42% drawdown. QQQ's worst was 83%. I'd rather lose 42 cents and have the chance to make them back than lose 83 cents and spend a decade waiting.

The rule is not free. It will underperform QQQ in years when QQQ is in mania mode and nothing crashes. We saw this in 1999, when QQQ ran up 79% in nine months and the rule only made 26%. We saw it again from 2017 to 2020, when a small handful of growth stocks were doing all the heavy lifting in the index. If the next twenty years turn out to be a long calm bull market with no real corrections, you would have been better off in QQQ than in this rule. The rule is built to survive bad weather, not to win blue-sky days. If you cannot stomach being the person at the dinner party who didn't own whatever stock the magazine cover featured, this strategy will be painful to hold.