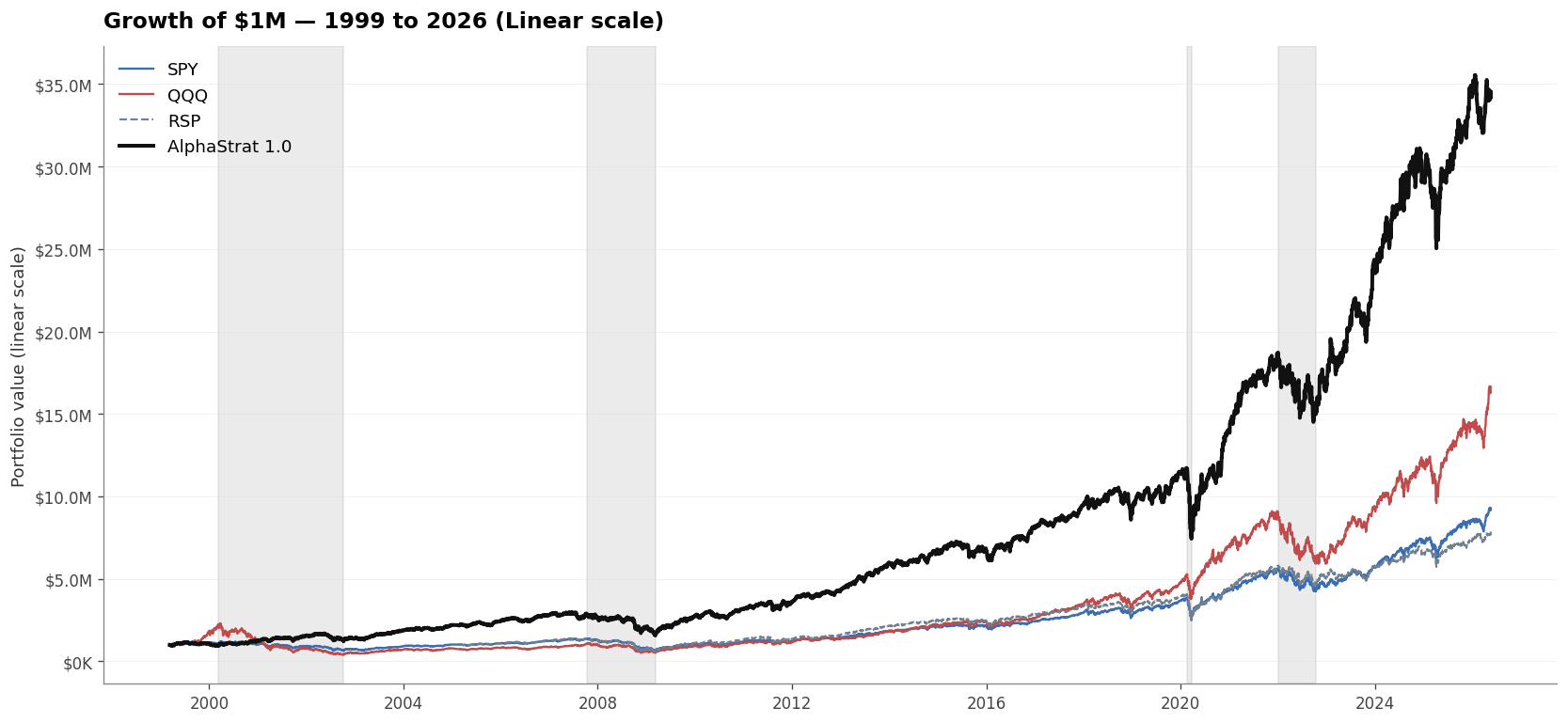

Every backtest is a small story told in a way that flatters its author. Here is everything we know we’re leaving out, and the rough size of each lie. Read this section twice.

1. The dead are missing

The universe is built from the US large-caps that exist today. Enron is not in it. Neither is Lehman Brothers, WorldCom, Bear Stearns, Washington Mutual, Countrywide, Sun Micro, or Pets.com. A correctly-built historical universe that included these tombstones would, in our estimate, knock 1 to 3 percentage points a year off the CAGR we show. We’re working on fixing this in a future version.

2. Yesterday is not tomorrow

These numbers are simulated. Nobody made any of this money. The next 27 years will look nothing like the last 27 years, and the particular pattern of value rotations and tech booms that this strategy navigated may not recur in the same way. The honest answer to "will this work going forward?" is "the principles are sound; the magnitude is unknowable." Anyone telling you otherwise is selling something.

3. Sector risk is reduced, not eliminated

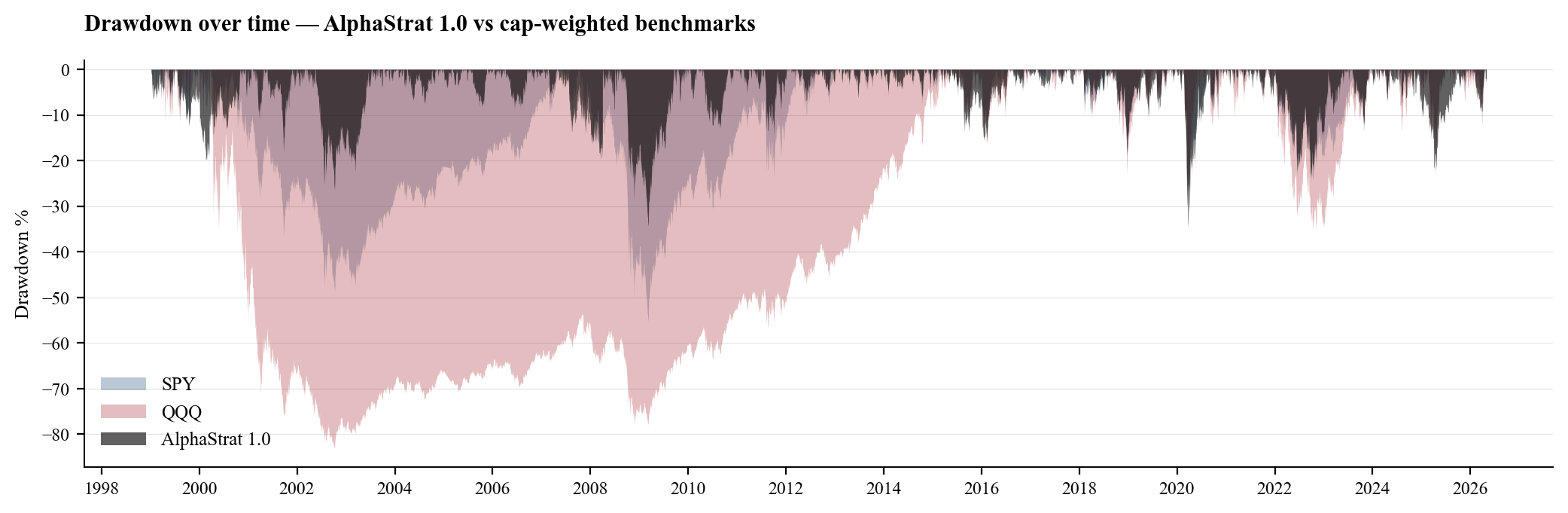

No sector ever gets more than five of the thirty slots, which caps it at about 17% of the book. That stops us from being all in on banks the way an uncapped value strategy can be. But a credit shock that hits banks, REITs, and leveraged infrastructure all at once can still produce a correlated drawdown across positions that look diversified.

4. The trading costs are optimistic

10 basis points of one-way slippage. No commissions, no market impact. That is generous for $1B+ stocks and fine for an individual investor at this size. It would be wrong if a billion dollars tried to run this strategy.

5. Cash is treated as a free option

Uninvested cash is assumed to earn the day-over-day total return on short-term Treasuries. That overstates what you’d get on real cash sitting in a brokerage account, and understates the borrow cost if you ever ran the strategy on margin. The size of this lie is small but it’s nonzero.

6. The IRS gets paid first

This is the most important paragraph in the report and you should not skip it. Every number we’ve shown you so far is before tax. Rebalancing four times a year turns the portfolio over at roughly 75 to 90% a year, which means almost every gain we realize is held under twelve months. In a US taxable account that gets taxed as ordinary income. Your federal rate is whatever your last dollar of wages is taxed at, plus the 3.8% net investment income tax for high earners, plus your state. The S&P 500 in a buy-and-hold account has almost no realized gains until you sell. We have a lot of them, every quarter, forever. That is a structural tax disadvantage, and no amount of clever ranking fixes it.

Here is what the 14.57% gross CAGR turns into after the tax man takes his share, at different brackets, assuming 78% turnover:

| Account Type / Tax Bracket |

Estimated CAGR |

vs SPY After-Tax (Δ) |

| Tax-advantaged (IRA / 401(k) / endowment / foundation) |

14.57% |

+6.76 pp |

| Taxable — moderate bracket (~30%) |

11.16% |

+3.35 pp |

| Taxable — top federal + NIIT (40.8%) |

9.93% |

+2.12 pp |

| Taxable — top federal + state (e.g. CA, ~51%) |

8.78% |

+0.96 pp |

The strategy belongs in a tax-advantaged account—an IRA, a 401(k), an endowment, a foundation. In a taxable account at the top California bracket the edge over SPY narrows to a sliver. Your real result will depend on your bracket, your state, whether you can harvest losses against the realized gains, and whether any positions happen to survive long enough to qualify for long-term treatment. Run the numbers with your accountant before you do anything.