Paysign, Inc. to Present at the Planet MicroCap Las Vegas 2026

Paysign, Inc. (NASDAQ: [url="]PAYS[/url]), a leading provider of patient affordability programs, donor compensation solutions, engagement and management platfo

Paysign, Inc. (NASDAQ: [url="]PAYS[/url]), a leading provider of patient affordability programs, donor compensation solutions, engagement and management platfo

HENDERSON, Nev.--(BUSINESS WIRE)--Paysign, Inc. to Present at the Planet MicroCap Las Vegas 2026.

Paysign, Inc. (NASDAQ: [url="]PAYS[/url]), a leading provider of patient affordability programs, donor compensation solutions, engagement and management platfo

HENDERSON, Nev.--(BUSINESS WIRE)--Paysign, Inc. to Present at the Barrington Research Virtual Spring Investment Conference.

Paysign handily beat Wall Street analysts in the first quarter but didn't raise guidance. The stock looks cheap.

Paysign, Inc. (PAYS) Q1 2026 Earnings Call Transcript

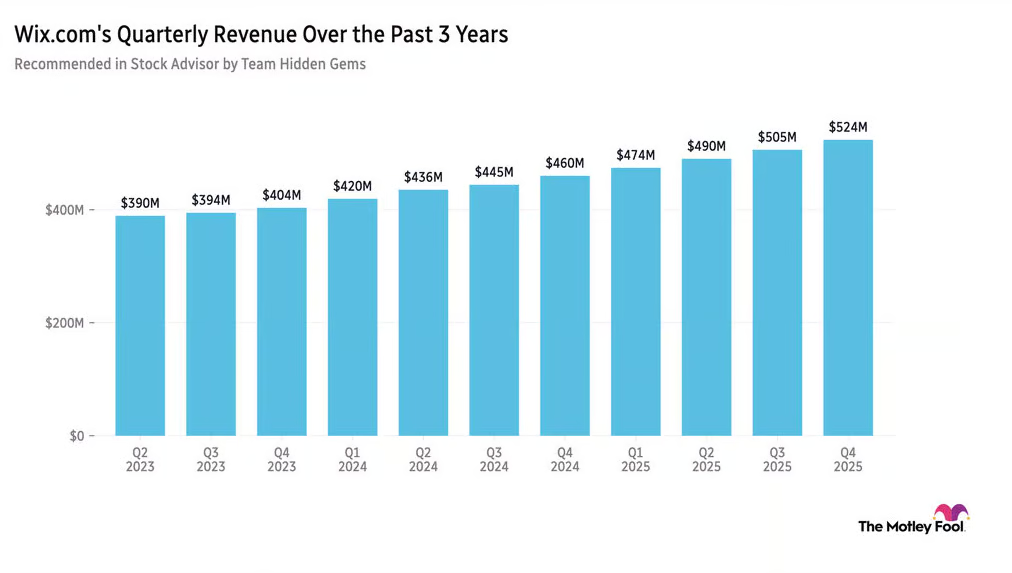

Wix.com revenue growth continues, PaySign beats Q1 management guidance, and more

Paysign NASDAQ: PAYS reported what executives described as the strongest start to a year in the company's history, with first-quarter 2026 revenue rising 50.8% year over year to $28 million and profitability expanding sharply as its patient affordability business became its largest revenue contributor.

HENDERSON, Nev.--(BUSINESS WIRE)--Paysign's Patient Affordability Drives 51% Revenue Growth and Significant Margin Expansion for First Quarter 2026.

HENDERSON, Nev.--(BUSINESS WIRE)--Paysign to Host First Quarter 2026 Earnings Call.

Paysign is evolving beyond a niche prepaid card processor, with patient affordability now driving higher-margin growth. 2025 results highlight a 40.5% revenue increase to $82M, with pharma revenue surging to $33.9M and gross margin expanding to 59.4%. PAYS trades above peer sales multiples, reflecting its shift to a high-value workflow business, while price-to-cash flow remains attractive if cash conversion holds.

Paysign remains a buy, supported by strong performance in both Plasma Centers and hypergrowth in Patient Affordability. PAYS's Plasma Center segment holds a 50% market share, adding 115 new centers in FY25, despite revenue per center declining due to plasma surplus. That surplus can disappear, and the Plasma segment can benefit from the BECS, generating high-margin SaaS subscription revenue.

Paysign (NASDAQ: PAYS) reported fourth-quarter and full-year 2025 results that management said showed "continued strength and exceptional growth" across key metrics, driven primarily by rapid expansion in its patient affordability platform and improving operating leverage. Full-year 2025 results and margin improvement For full-year 2025, the company said revenue increased 40.5% to $82.0 million. Net income rose

Paysign posted Q4 earnings that were in line with Wall Street's target and sales that beat expectations. The company's forward guidance is spurring huge gains for the stock.

Paysign, Inc. (PAYS) Q4 2025 Earnings Call Transcript

HENDERSON, Nev.--(BUSINESS WIRE)--Paysign, Inc. Reports Fourth Quarter and Full-Year 2025 Financial Results.

Paysign, Inc. (NASDAQ: PAYS - Get Free Report) has been assigned an average rating of "Moderate Buy" from the five research firms that are covering the firm, MarketBeat reports. One equities research analyst has rated the stock with a hold recommendation and four have assigned a buy recommendation to the company. The average twelve-month target price

Marqeta (NASDAQ: MQ - Get Free Report) and Paysign (NASDAQ: PAYS - Get Free Report) are both small-cap business services companies, but which is the superior investment? We will contrast the two companies based on the strength of their analyst recommendations, risk, valuation, earnings, profitability, institutional ownership and dividends. Profitability This table compares Marqeta and Paysign's net

HENDERSON, Nev.--(BUSINESS WIRE)--Paysign to Host Fourth Quarter and Full Year 2025 Earnings Call.

Shares of Paysign, Inc. (NASDAQ: PAYS - Get Free Report) have received an average rating of "Moderate Buy" from the five ratings firms that are currently covering the stock, Marketbeat.com reports. One investment analyst has rated the stock with a hold rating and four have given a buy rating to the company. The average 1-year target